How much will a long-term care insurance policy cost you? An independent agent who you can trust can answer these questions with quotes that have numbers for you to compare the top insurance companies with. Premium rates range based on your health, age, career and or hobbies, and how much coverage you need. An agent is an important part of this process because for every one person there can be hundreds of policy options and premium price ranges. An agent can narrow these down and show you the best options available for your needs. An agent will show you the numbers that work specifically for your individual wants and needs.

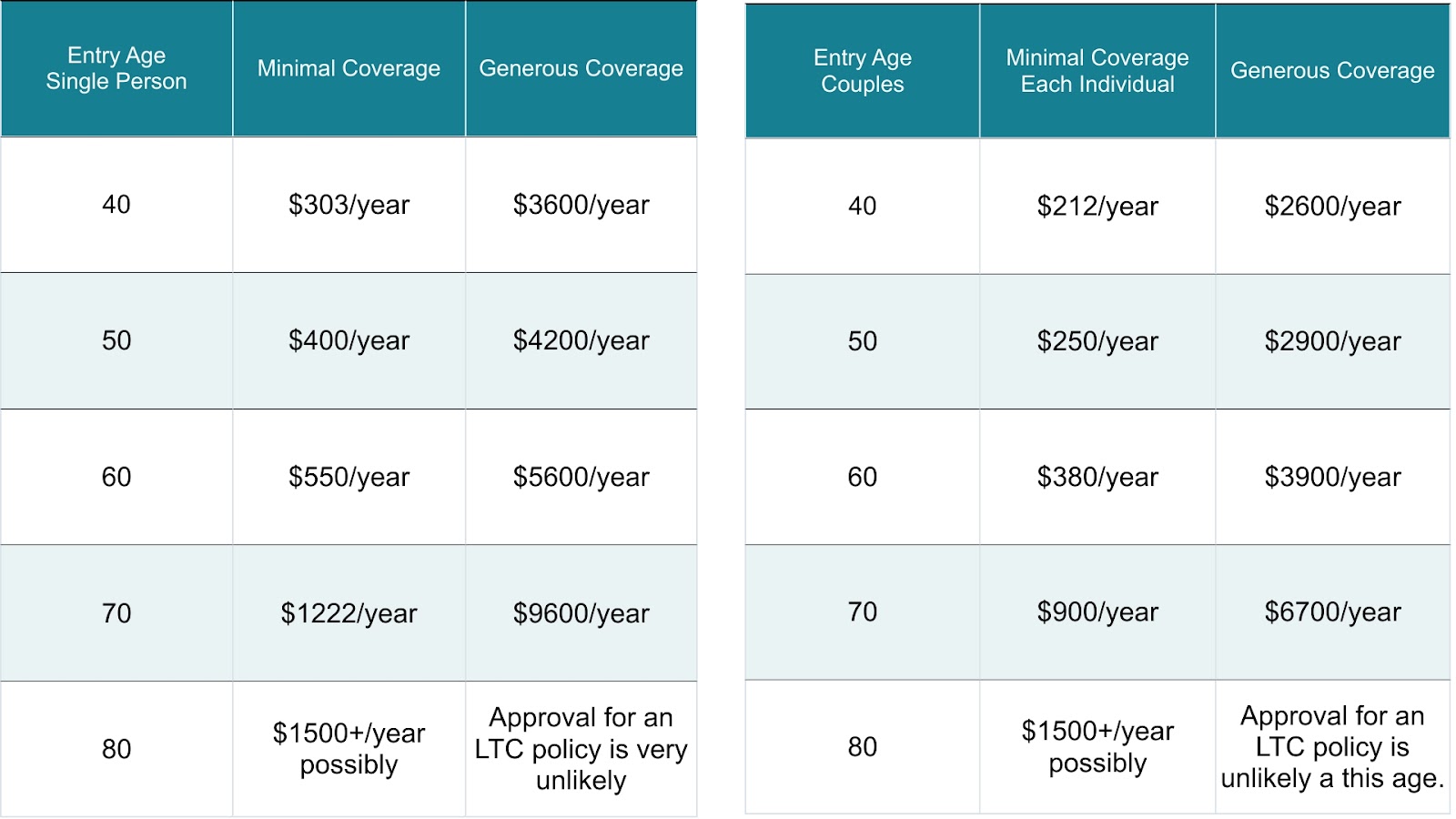

Here is an example of some synthetic numbers we have created for you to look at:

Minimal Coverage: Spouse and or Preferred Discount / $100 per day maximum daily benefit / 2 year benefit period / 90 day elimination period / No 5% inflation adjustments in the graph.

Generous Coverage: May include facility/homecare at 100% / $250 per day maximum daily benefits / Lifetime unlimited benefit period / 90 day elimination period / 5% inflation adjustment.

These benefits are simply examples and do not reflect any one person or specific company or state. They are for educational purposes and are only to show the large range of possible premium rates.

Here are a few definitions of benefit options that will affect the premium costs:

Maximum Daily Benefit: $50-$400 / The amount you want the company to payout per day for your daily care you believe you’ll need.

Elimination Period: The elimination period is the number of days you are willing to pay for your own care out of pocket. 0, 20, 30, 60, 90 or 100 plus days – options of how soon you could start receiving payments once you become eligible. The longer the elimination period the lower the [premium is for you.

Benefit Period: The length of time you would like to receive benefits for your care. 2, 3, 4, 5, or unlimited years.

3% Inflation Adjustment: The maximum daily benefit percentage. Increases the value of your benefit 3% each policy year to keep up with the rising prices of care costs. Asking for none or 5% inflation adjustment would change the premium costs.

Health: Your personal health can be a very large factor in the decision of the price of your policy. A healthier person will pay less than someone who has health complications, even if there are small issues.

Now that you know some of what goes into the cost of your LTC coverage, you can go to your agent and let them know what you believe you’ll need in coverage and they will create quotes that will work best for you and your needs. Inevitably, your health and personal choices of coverage needed are what will set your policy aside from everyone else making it impossible for anyone else to have a policy exactly like yours.