History was made on January 1st, 1997 as a result of the Kennedy/Kasselbum welfare and health care reform. Legislation signed this law in August of 1996 making it so premiums paid for “tax-qualified” long term care insurance receive tax-favored status. Tax-favored status is granted to all long term care insurance policies issued before January 1st, 1997, if they are complying with their states standards. Almost all policies bought before December 31st, 1996 were grandfathered in and are considered tax-qualified.

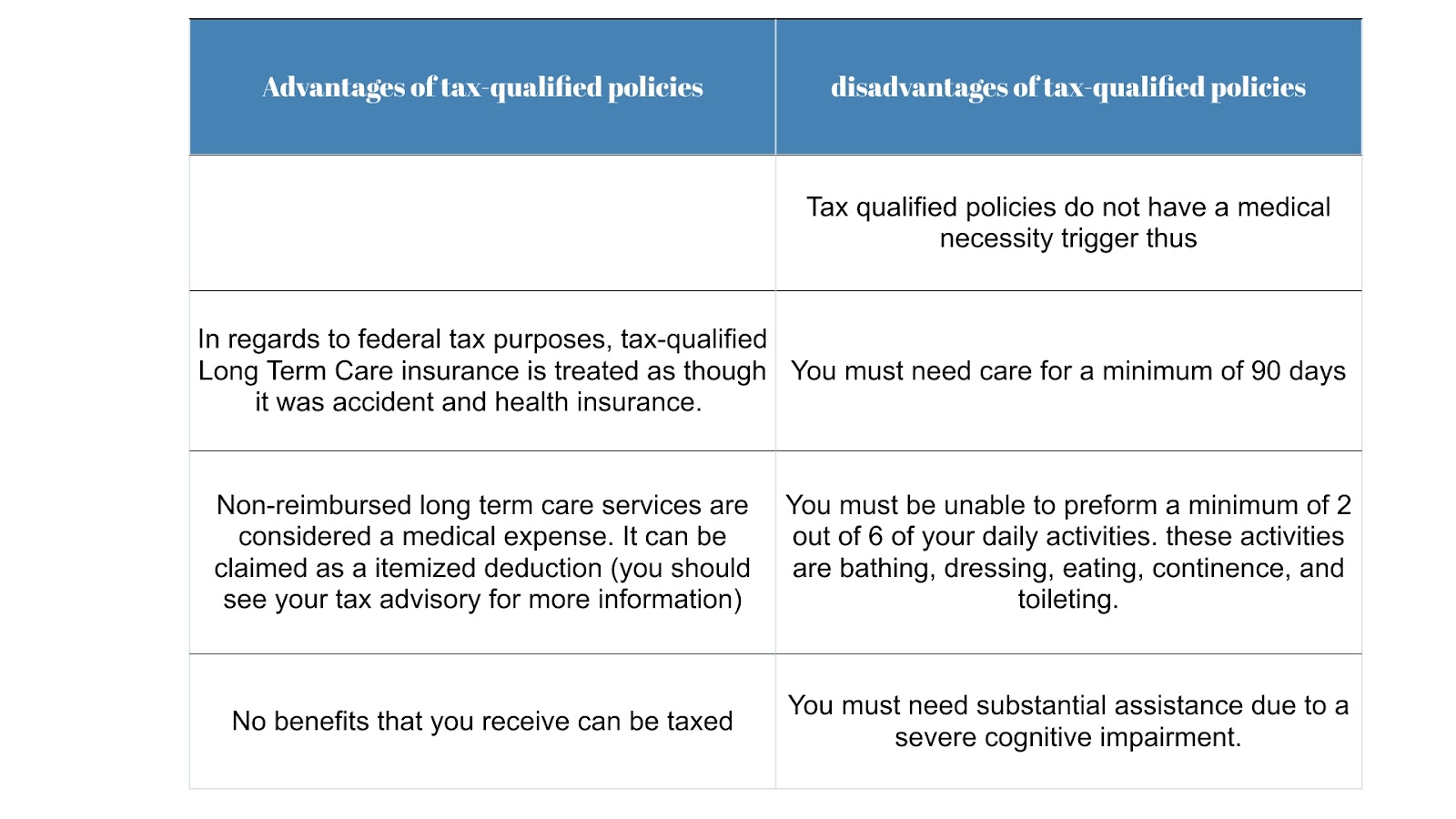

Here are some pros and cons of tax-qualified policies:

Uncle Sam Telling Americans to Wake Up

Tax-favored status essentially indicates that the government as a whole recognizes its inability to cover the cost of long term care through entitlement programs such as medicare and medicaid. It also shows that for the most part funding of long term care is a personal responsibility.

So tax-qualified or non tax-qualified is the question. Generally all benefits paid in accordance with a long term care policy are tax-free. In addition to that your premiums are deductible as a medical expense, up to a certain percentage. So what is the big difference? A non-qualified policy has no tax deduction for the premiums you pay.

Your tax deductions are determined by your age. Usually you will have to itemize your deductions and have expenses that exceed the AGI threshold to qualify. There is one exception for those who are self-employed individuals. Self-employed individuals can deduct 100% of his or her out-of-pocket long term care insurance premiums up to the eligible premium amount set by the government.

If you are a single (alone/not married) individual after 70 years old, up to $5,430 (2020 limit) can be counted towards deductible medical expenses.This is only if you have a tax-qualified plan. If you are married the amount could be double the amount of a single person, at $10,860. (2020 numbers) When on a strict budget this can be very big for some people and after the age of 70 your income is most likely going to be lower and one of not both of the couple will need medical, dental, or vision expenses. LTC policies can help by reducing your taxes.

At the end of the day whether you wish to sign up for a tax-qualified plan or not is entirely your decision, but it seems clear to me that a tax-qualified plan is the one that saves you the most money in the long run, especially after 70 years old.