Who do you usually see when you visit a nursing home? Who are most of the nursing home residents, men or women? It is most likely that your trip to a local nursing home matches the statistic of the nation, stating that the majority of nursing home residents are older, single, women. Women on average live longer than men causing them to need nursing homes and or assisted living help longer than men. Women live longer than men, but that also means women will need more long care insurance to protect themselves from financial ruin in old age.

A study produced by Medicaid, in New York, revealed the following statistics:

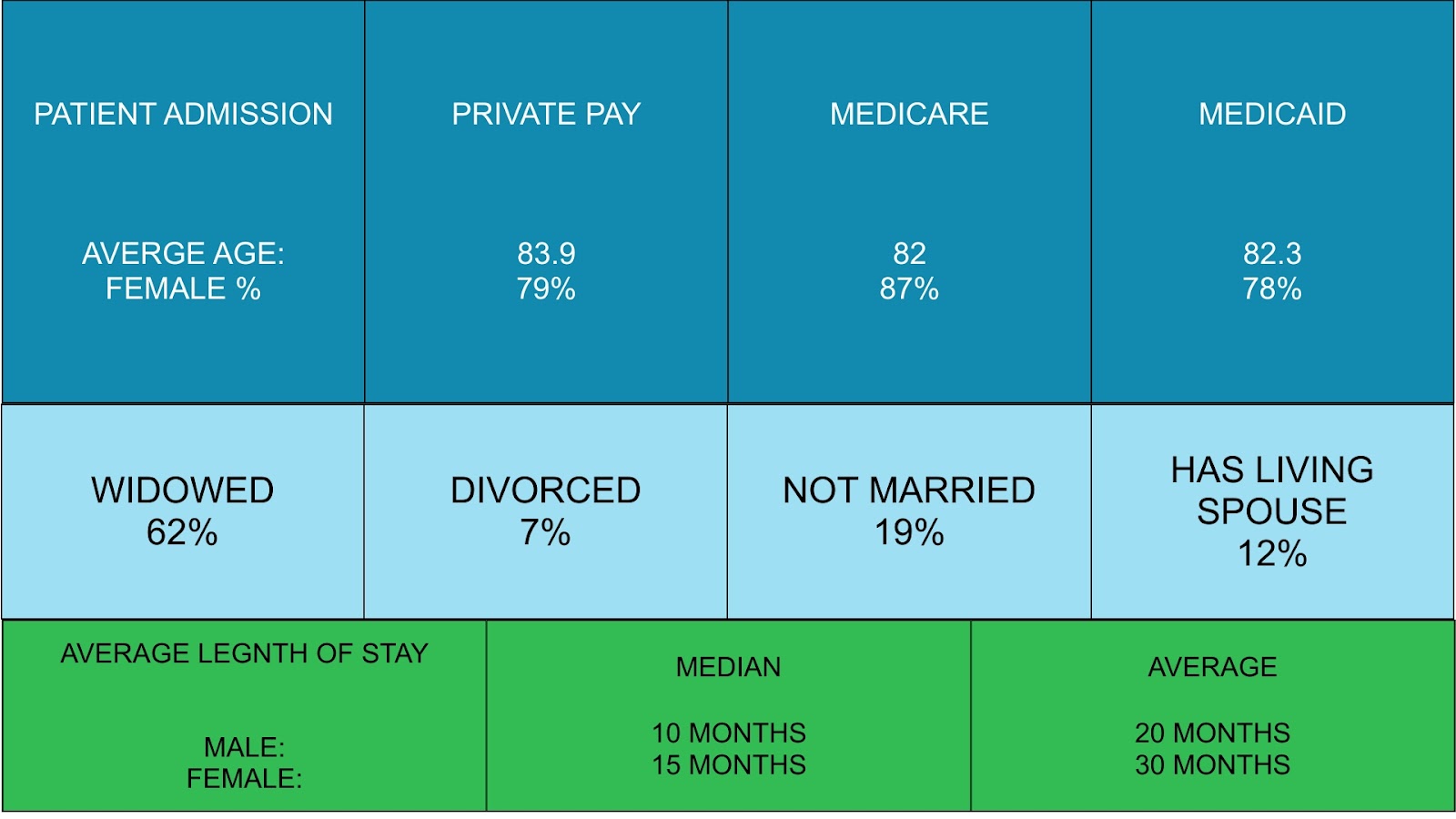

Graph Summary

Approximately 80% of residents in nursing homes are women and the average admission age for women in nursing homes is 82 years old. The graph also displays that at advanced ages most women are alone/single and this is partly because women outlive their male counterparts. Women spend 50% more of their lifetime in nursing homes than men do and that is one reason women need to look into long-term care insurance to help balance out the cost of needing care for longer.

Who Needs LTC for Longer?

It has been proven true, that on average women live longer than men and when men become ill their wife or significant other often takes care of them until they die, and then women enter into nursing homes once they become ill or too old to take care of themselves. If this is not the case then a man’s wife may admit him into a nursing home if she is already not physically or mentally able to care for him, but he would die shortly after becoming ill while under nursing home care statistically and thereafter the wife will do the same for herself, but live in the home for a longer period then her spouse had.

In Conclusion

Long-term care is a problem for women to worry about. Women either take care of their husbands or admit them and will usually eventually need to be admitted themselves. Women take on the most risk and it is no surprise most women start the long-term care insurance process for either themselves or their spouses much more often than their male counterparts. Women need to take the first step in making sure they are covered no matter how much longer they live than their counterparts may. How will you cover these expenses if you don’t plan? That’s where LTC insurance helps. You start investing now and when you need the care your long-term care provider either pays the bills or sends you a check for the costs.