Can an investment side-fund be better than long term care insurance? In short, not exactly. Insurance is never an ‘investment’ because it is protection for your investments and assets. Insurance gives you a growth for your investment portfolio and pure insurance is never meant to provide you with a “return on investment”, but instead covers the cost of care needed during your golden age or because of a sudden disability often due to strokes or falls in older age. Long or short term insurance can provide you more options for how you will receive care when needed without draining your assets.

Insurance is an “expense” which you take on in order to protect financially against the possible negative consequences of being unprepared for the cost of care needed at an older age. It cannot beat an investment in the form of “return of investment”, but without long term care insurance your investments are at risk of being drained by the cost of care and may prove your investments to be for naught in the long run.

Once again, insurance is directly viewed as an expense. Just like airbags, seat belts, health insurance, and even first aid kits and sunscreen; it is there for you in the event you are in need of it. At that point it is beating an investment butt and is there to save the day. In the aspect of long term care insurance, what is being protected is your investments and family assets, as well as the security of quality care and peace of mind for the whole family.

You fund it and hope that you’ll never be in need of it. The reason it is growing in popularity though, is because as we as a community are living longer, our needs for long term care have been growing as well. Everyone should hope that long term care insurance is “money down the drain”, but often towards the end of life it is more and more likely long term care will be needed.

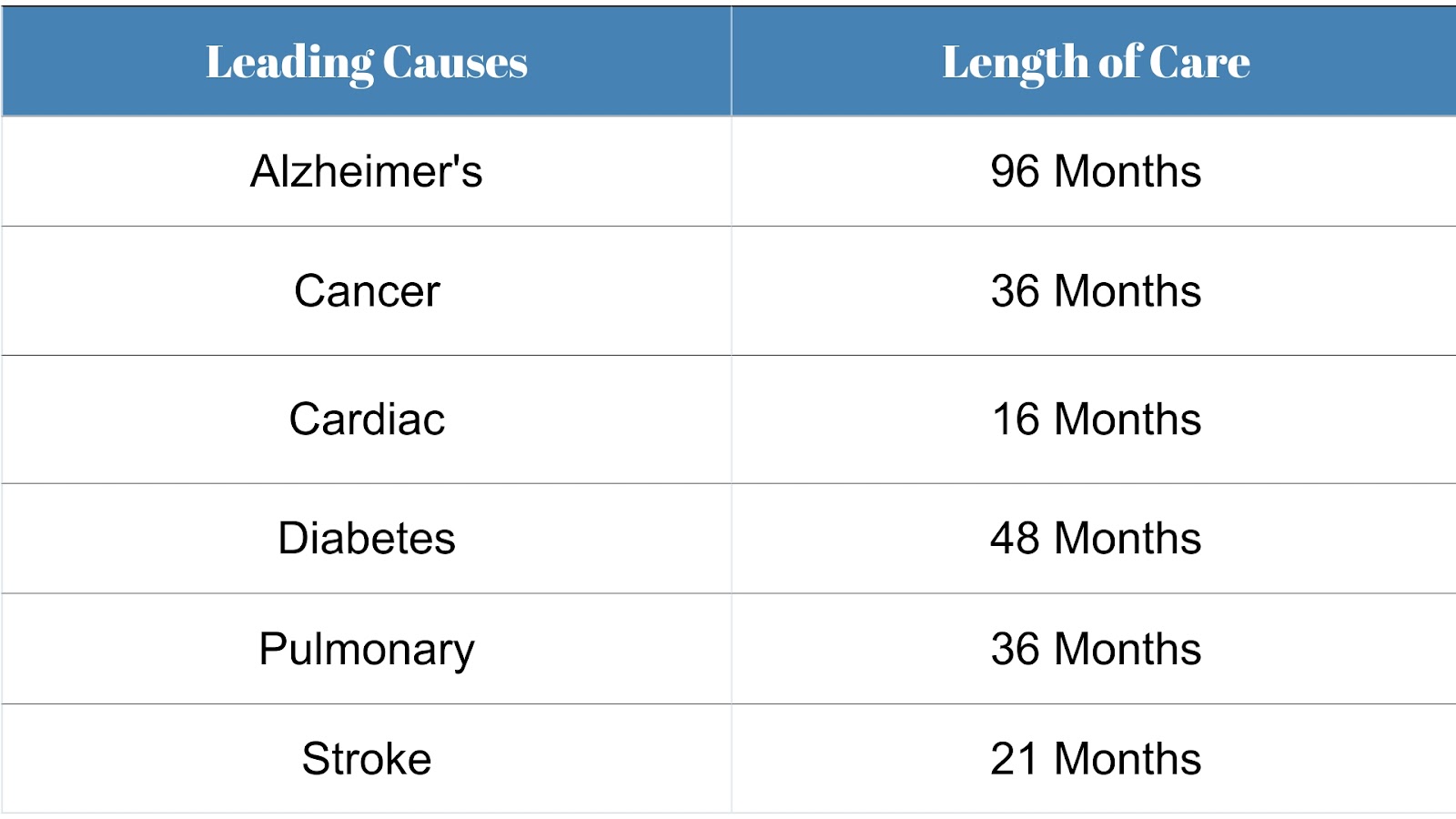

There is a nearly 50% chance of needing 24-hour skilled nursing care, due to medical conditions and here are the statistics.

Nursing home care cost varies by state, but the average low is $40,000 and average high is $200,000 per year. These figures inflate by at least 5% annually. So if you needed care ten years from now you could guess that your average cost for a private room would be approximately $1,600,000. That’s a large amount of money to pay out of pocket, even if you have had amazing luck in the stock markets. For many paying this out of pocket would be impossible and that’s where long term life insurance beats investments. No one wants to go to a nursing home, smart people want to be able to afford alternatives.

You may still be tempted to compare the numbers, but I’ve done the comparison for you and no matter what age you begin, investing never works as well as insurance.